By Zongyuan Zoe Liu

Why Beijing Won’t Give Up on a Failing Model

The Chinese economy is stuck. Following Beijing’s decision, in late 2022, to abruptly end its draconian “zero COVID” policy, many observers assumed that China’s growth engine would rapidly reignite. After years of pandemic lockdowns that brought some economic sectors to a virtual halt, reopening the country was supposed to spark a major comeback. Instead, the recovery has faltered, with sluggish GDP performance, sagging consumer confidence, growing clashes with the West, and a collapse in property prices that has caused some of China’s largest companies to default. In July 2024, Chinese official data revealed that GDP growth was falling behind the government’s target of about five percent. The government has finally let the Chinese people leave their homes, but it cannot command the economy to return to its former strength.

To account for this bleak picture, Western observers have put forward a variety of explanations. Among them are China’s sustained real estate crisis, its rapidly aging population, and Chinese leader Xi Jinping’s tightening grip on the economy and extreme response to the pandemic. But there is a more enduring driver of the present stasis, one that runs deeper than Xi’s growing authoritarianism or the effects of a crashing property market: a decades-old economic strategy that privileges industrial production over all else, an approach that, over time, has resulted in enormous structural overcapacity. For years, Beijing’s industrial policies have led to overinvestment in production facilities in sectors from raw materials to emerging technologies such as batteries and robots, often saddling Chinese cities and firms with huge debt burdens in the process.

Simply put, in many crucial economic sectors, China is producing far more output than it, or foreign markets, can sustainably absorb. As a result, the Chinese economy runs the risk of getting caught in a doom loop of falling prices, insolvency, factory closures, and, ultimately, job losses. Shrinking profits have forced producers to further increase output and more heavily discount their wares in order to generate cash to service their debts. Moreover, as factories are forced to close and industries consolidate, the firms left standing are not necessarily the most efficient or most profitable. Rather, the survivors tend to be those with the best access to government subsidies and cheap financing.

Since the mid-2010s, the problem has become a destabilizing force in international trade, as well. By creating a glut of supply in the global market for many goods, Chinese firms are pushing prices below the break-even point for producers in other countries. In December 2023, European Commission President Ursula von der Leyen warned that excess Chinese production was causing “unsustainable” trade imbalances and accused Beijing of engaging in unfair trade practices by offloading ever-greater quantities of Chinese products onto the European market at cutthroat prices. In April, U.S. Treasury Secretary Janet Yellen warned that China’s overinvestment in steel, electric vehicles, and many other goods was threatening to cause “economic dislocation” around the globe. “China is now simply too large for the rest of the world to absorb this enormous capacity,” Yellen said.

Despite vehement denials by Beijing, Chinese industrial policy has for decades led to recurring cycles of overcapacity. At home, factories in government-designated priority sectors of the economy routinely sell products below cost in order to satisfy local and national political goals. And Beijing has regularly raised production targets for many goods, even when current levels already exceed demand. Partly, this stems from a long tradition of economic planning that has given enormous emphasis to industrial production and infrastructure development while virtually ignoring household consumption. This oversight does not stem from ignorance or miscalculation; rather, it reflects the Chinese Communist Party’s long-standing economic vision.

As the party sees it, consumption is an individualistic distraction that threatens to divert resources away from China’s core economic strength: its industrial base. According to party orthodoxy, China’s economic advantage derives from its low consumption and high savings rates, which generate capital that the state-controlled banking system can funnel into industrial enterprises. This system also reinforces political stability by embedding the party hierarchy into every economic sector. Because China’s bloated industrial base is dependent on cheap financing to survive—financing that the Chinese leadership can restrict at any time—the business elite is tightly bound, and even subservient, to the interests of the party. In the West, money influences politics, but in China it is the opposite: politics influences money. The Chinese economy clearly needs to strike a new balance between investment and consumption, but Beijing is unlikely to make this shift because it depends on the political control it gets from production-intensive economic policy.

For the West, China’s overcapacity problem presents a long-term challenge that can’t be solved simply by erecting new trade barriers. For one thing, even if the United States and Europe were able to significantly limit the amount of Chinese goods reaching Western markets, it would not unravel the structural inefficiencies that have accumulated in China over decades of privileging industrial investment and production goals. Any course correction could take years of sustained Chinese policy to be successful. For another, Xi’s growing emphasis on making China economically self-sufficient—a strategy that is itself a response to perceived efforts by the West to isolate the country economically—has increased, rather than decreased, the pressures leading to overproduction. Moreover, efforts by Washington to prevent Beijing from flooding the United States with cheap goods in key sectors are only likely to create new inefficiencies within the U.S. economy, even as they shift China’s overproduction problem to other international markets.

To craft a better approach, Western leaders and policymakers would do well to understand the deeper forces driving China’s overcapacity and make sure that their own policies are not making it worse. Rather than seeking to further isolate China, the West should take steps to keep Beijing firmly within the global trading system, using the incentives of the global market to steer China toward more balanced growth and less heavy-handed industrial policies. In the absence of such a strategy, the West could face a China that is increasingly unrestrained by international economic ties and prepared to double down on its state-led production strategy, even at the risk of harming the global economy and stunting its own prosperity.

FACTORY DEFECTS

The structural issues underlying China’s economic stasis are not the result of recent policy choices. They stem directly from the lopsided industrial strategy that took shape in the earliest years of China’s reform era, four decades ago. China’s sixth five-year plan (1981–85) was the first to be instituted after Chinese leader Deng Xiaoping opened up the Chinese economy. Although the document ran to more than 100 pages, nearly all of it was devoted to developing China’s industrial sector, expanding international trade, and advancing technology; only a single page was given to the topic of increasing income and consumption. Despite vast technological changes and an almost unrecognizably different global market, the party’s emphasis on China’s industrial base remains remarkably similar today. The 14th five-year plan (2021–25) offers detailed targets for economic growth, R & D investment, patent achievement, and food and energy production—but apart from a few other sparse references, household consumption is relegated to a single paragraph.

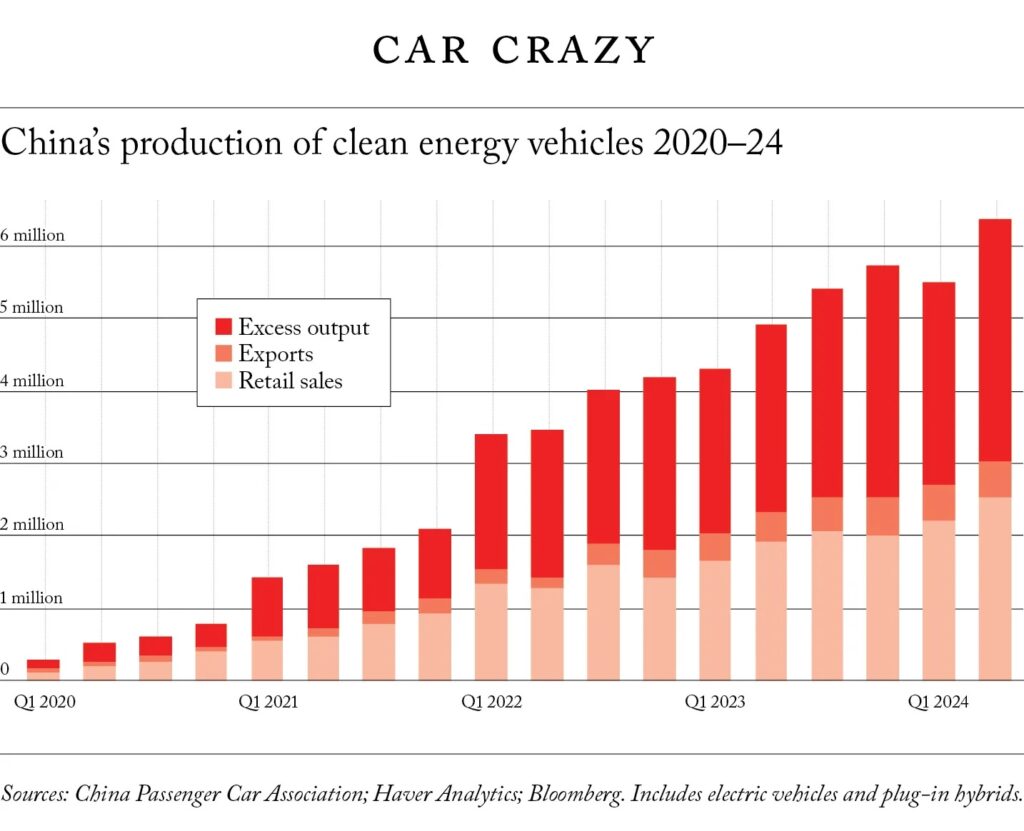

In prioritizing industrial output, China’s economic planners assume that Chinese producers will always be able to offload excess supply in the global market and reap cash from foreign sales. In practice, however, they have created vast overinvestment in production across sectors in which the domestic market is already saturated and foreign governments are wary of Chinese supply chain dominance. In the early years of the twenty-first century, it was Chinese steel, with the country’s surplus capacity eventually exceeding the entire steel output of Germany, Japan, and the United States combined. More recently, China has ended up with similar excesses in coal, aluminum, glass, cement, robotic equipment, electric-vehicle batteries, and other materials. Chinese factories are now able to produce every year twice as many solar panels as the world can put to use.

For the global economy, China’s chronic overcapacity has far-reaching impacts. With electric vehicles, for instance, carmakers in Europe are already facing stiff competition from cheap Chinese imports. Factories in this and other emerging technology sectors in the West may close or, worse, never get built. Moreover, high-value manufacturing industries have economic effects that go far beyond their own activities; they generate service-sector employment and are vital to sustaining the kinds of pools of local talent that are needed to spur innovation and technological breakthroughs. In China’s domestic market, overcapacity issues have provoked a brutal price war in some industries that is hampering profits and devouring capital. According to government statistics, 27 percent of Chinese automobile manufacturers were unprofitable in May; at one point last year, the figure reached 32 percent. Overproduction throughout the economy has also depressed prices generally, causing inflation to hover near zero and the debt service ratio for the private nonfinancial sector—the ratio of total debt payments to disposable income—to climb to an all-time high. These trends have eroded consumer confidence, leading to further declines in domestic consumption and increasing the risk of China sliding into a deflationary trap.

When Beijing’s economic planners do talk about consumption, they tend to do so in relation to industrial aims. In its brief discussion of the subject, the current five-year plan states that consumption should be steered specifically toward goods that align with Beijing’s industrial priorities: automobiles, electronics, digital products, and smart appliances. Analogously, although China’s vibrant e-commerce sector might suggest a plethora of consumer choices, in reality, major platforms such as Alibaba, Pinduoduo, and Shein compete fiercely to sell the same commoditized products. In other words, the illusion of consumer choice masks a domestic market that is overwhelmingly shaped by the state’s industrial priorities rather than by individual preferences.

This is also reflected in policy initiatives aimed at boosting consumer spending. Consider the government’s recent effort to promote goods replacement. According to a March 2024 action plan, the Ministry of Commerce, together with other Chinese government agencies, has offered subsidies to consumers who trade in old automobiles, home appliances, and fixtures for new models. On paper, the plan loosely resembles the “cash for clunkers” program that Washington introduced during the 2008 recession to help the U.S. car industry. But the plan lacks specific details and relies on local authorities for implementation, rendering it largely ineffective; it has notably failed to lift the prices of durable goods. Although the government can influence the dynamics of supply and demand in China’s consumer markets, it cannot compel people to spend or punish them if they do not. When income growth slows, people naturally tighten their purses, delay big purchases, and try to make do for longer with older equipment. Paradoxically, the drag that overcapacity has placed on the economy overall means that the government’s efforts to direct consumption are making people even less likely to spend.

DEBT COLLECTORS

At the center of Beijing’s overcapacity problem is the burden placed on local authorities to develop China’s industrial base. Top-down industrial plans are designed to reward the cities and regions that can deliver the most GDP growth, by providing incentives to local officials to allocate capital and subsidies to prioritized sectors. As the scholar Mary Gallagher has observed, Beijing has fanned the flames by using social campaigns such as “common prosperity”—a concept Chinese leader Mao Zedong first proposed in 1953 and that Xi revived at a party meeting in 2021—to spur local industrial development. These planning directives and campaigns put enormous pressure on local party chiefs to achieve rapid results, which they may see as crucial for promotion within the party. Consequently, these officials have strong incentives to make highly leveraged investments in priority sectors, irrespective of whether these moves are likely to be profitable.

This phenomenon has fueled risky financing practices by local governments across China. In order to encourage local initiative, Beijing often does not provide financing: instead, it gives local officials broad discretion to arrange off-balance-sheet investment vehicles with the help of regional banks to fund projects in priority sectors, with the national government limiting itself to specifying which types of local financing options are prohibited. About 30 percent of China’s infrastructure spending comes from these investment vehicles; without them, local officials simply cannot do the projects that will win them praise within the party. Inevitably, this approach has led to not only huge industrial overcapacity but also enormous levels of local government debt. According to an investigation by The Wall Street Journal, in July, the total amount of off-the-book debts held by local governments across China now stands at between $7 trillion and $11 trillion, with as much as $800 billion at risk of default.

Although the scale of debt may be worse now, the problem is not new. Ever since China’s 1994 fiscal reform, which allowed local governments to retain a share of the tax revenue they collected but reduced the fiscal transfers they received from Beijing, local governments have been under chronic financial strain. They have struggled to meet their dual mandate of promoting local GDP growth and providing public services with limited resources. By centralizing financial power at the national level and offloading infrastructure and social service expenditures to regions and municipalities, Beijing’s policies have driven local governments into debt. What’s more, by stressing rapid growth performance, Beijing has pushed local officials to favor quickly executed capital projects in industries of national priority. As a further incentive, Beijing sometimes offers limited fiscal support for projects in priority sectors and helps facilitate approvals for local governments to secure financing. Ultimately, the local government bears the financial risk, and the success or failure of the project rests on the shoulders of the party’s local chief, which leads to distorted results.

A larger problem with China’s reliance on local government to implement industrial policy is that it causes cities and regions across the country to compete in the same sectors rather than complement each other or play to their own strengths. Thus, for more than two decades, Chinese provinces—from Xinjiang in the west to Shanghai in the east, from Heilongjiang in the north to Hainan in the south—have, with very little coordination between them, established factories in the same government-designated priority industries, driven by provincial and local officials’ efforts to outperform their peers. Inevitably, this domestic competition has led to overcapacity and high levels of debt, even in industries in which China has gained global market dominance.

“Every year, Chinese factories produce twice as many solar panels as the world can use”.

Take solar panels. In 2010, China’s State Council announced that strategic emerging industries, including solar power, should account for 15 percent of national GDP by 2020. Within two years, 31 of China’s 34 provinces had designated the solar-photovoltaic industry as a priority, half of all Chinese cities had made investments in the solar-PV industry, and more than 100 Chinese cities had built solar-PV industrial parks. Almost immediately, China’s PV output outstripped domestic demand, with the excess supply being exported to Europe and other areas of the world where governments were subsidizing solar-panel ownership. By 2013, both the United States and the European Union imposed antidumping tariffs on Chinese PV manufacturers. By 2022, China’s own installed solar-PV capacity was greater than any other country’s, following its aggressive renewable energy build-out. But China’s electric grid cannot support additional solar capacity. With the domestic market completely saturated, solar manufacturers have resumed offloading as much of their wares as possible onto foreign markets. In August 2023, the U.S. Commerce Department found that Chinese PV producers were shipping products to Cambodia, Malaysia, Thailand, and Vietnam for minor processing procedures to avoid paying U.S. antidumping tariffs. China’s PV-production capacity, already double the global demand, is expected to grow by another 50 percent in 2025. This extreme oversupply caused the utilization rate in China’s finished solar power industry to plummet to just 23 percent in early 2024. Nevertheless, these factories continue operating because they need to raise cash to service their debt and cover fixed costs.

Another example is industrial robotics, which Beijing began prioritizing in 2015 as part of its Made in China 2025 strategy. At the time, there was a clear rationale for building a stronger domestic robotics industry: China had surpassed Japan to become the world’s largest buyer of industrial robots, accounting for about 20 percent of sales worldwide. Moreover, the plan seemed to achieve striking results. By 2017, there were more than 800 robotics companies and 40 robotics-focused industrial parks operating across at least 20 Chinese provinces. Yet this all-in effort did little to advance Chinese robotics technology, even as it created a huge industrial base. In order to meet Beijing’s ambitious production targets, local officials tended to invest in mature technologies that could be scaled quickly. Today, China has a large excess capacity in low-end robotics yet still lacks sufficient capacity in high-end autonomous robotics that require indigenous intellectual property.

Overcapacity in low-end production has plagued other Chinese tech industries, as well. The most recent example is artificial intelligence, which Beijing designated as a priority industry in its last two five-year plans. In August 2019, the government called for the creation of about 20 AI “pilot zones”—research parks that have a mandate to use local-government data for market testing. The aim is to exploit China’s two greatest strengths in the field: the ability to quickly build physical infrastructure, and thereby support the agglomeration of AI companies and talent, and the lack of constraints on how the government collects and shares personal data. Within two years, 17 Chinese cities had created such pilot zones, despite the disruption of the coronavirus pandemic and the government’s large-scale lockdowns. Each of these cities has also adopted action plans to induce further investments and data sharing.

On paper, the program seems impressive. China is now second only to the United States in AI investment. But the quality of actual AI research, especially in the field of generative AI, has been hindered by government censorship and a lack of indigenous intellectual property. In fact, many of the Chinese AI startups that have taken advantage of the strong government support are producing products that still fundamentally rely on models and hardware developed in the West. Similar to its initiatives in other emerging industries, Beijing risks wasting enormous capital on redundant investments that emphasize economies of scale rather than deep-rooted innovation.

RACE OF THE ZOMBIES

Paradoxically, even as Beijing’s industrial policy goals change, many of the features that drive overcapacity persist. Whenever the Chinese government prioritizes a new sector, duplicative investments by local governments inevitably fuel intense domestic competition. Firms and factories race to produce the same products and barely make any profit—a phenomenon known in China as nei juan, or involution. Rather than try to differentiate their products, firms will attempt to simply outproduce their rivals by expanding production as fast as possible and engaging in fierce price wars; there is little incentive to gain a competitive edge by improving corporate management or investing in R & D. At the same time, finite domestic demand forces firms to export excess inventory overseas, where it is subject to geopolitics and the fluctuations of global markets. Economic downturns in export destinations and rising trade tensions can stymie export growth and worsen overcapacity at home.

These dynamics all contribute to a vicious cycle: firms backed by bank loans and local government support must produce nonstop to maintain their cash flow. A production halt means no cash flow, prompting creditors to demand their money back. But as firms produce more, excess inventory grows and consumer prices drop further, causing firms to lose more money and require even more financial support from local governments and banks. And as companies go more deeply into debt, it becomes harder for them to pay it off, compounding the chance that they become “zombie companies,” essentially insolvent but able to generate just enough cash flow to meet their credit obligations. As China’s economy has stalled, the government has reduced the taxes and fees levied on firms as a way to spur growth—but that has reduced local government revenue, even as social-services expenditures and debt payments rise. In other words, the close financial relationship between local governments and the firms they support has created a wave of debt-fueled local GDP growth and left the economy in a hard-to-reverse overcapacity trap.

Yet even now, China shows few signs of reducing its reliance on debt. Xi has doubled down on his campaign for China to achieve technological self-sufficiency, amid intense geopolitical competition with the United States. As Beijing sees it, only by investing even more in strategic sectors can it protect itself from isolation or potential economic sanctions by the West. Thus, the government is concentrating on funding advanced manufacturing and strategic technologies and discouraging investments that it sees as distracting, such as in the property sector. In order to promote more indigenous high-end technology, Chinese policymakers have in recent years mobilized the entire banking system and set up dedicated loan programs to support research and innovation in prioritized sectors. The result has been a tendency to deepen, rather than correct, the structural problems leading to excess investment and production.

For example, in 2021, the China Development Bank created a special loan program for scientific and technological innovation and basic research. By May 2024, the bank had distributed more than $38 billion worth of loans to support critical, cutting-edge sectors, such as semiconductors, clean energy technology, biotech, and pharmaceuticals. In April, the People’s Bank of China, along with several government ministries, launched a $69 billion refinancing fund—to fuel a massive new round of lending by Chinese banks for projects aimed at scientific and technological innovation. Barely two months after the program’s launch, some 421 industrial facilities across the country were designated as “smart manufacturing” demonstration factories—a vague label given to factories that plan to integrate AI into their manufacturing processes. The program also announced investments in more than 10,000 provincial-level digital workshops and more than 4,500 AI-focused companies.

Beyond hitting top-line investment numbers, however, this campaign has few criteria for measuring actual success. Ironically, this new program’s stated goal of filling a financing gap for small and medium-sized enterprises that are working on innovations points to a larger shortcoming in Beijing’s economic management. For years, China’s industrial policy has tended to funnel resources to already mature companies; by contrast, with its massive effort to develop AI and other advanced technologies, the government has committed the financial resources to match the venture capital approach of the United States. Yet even here, China’s economic planners have failed to recognize that the real driving force of innovation is disruption. To truly foster this kind of creativity, entrepreneurs would need unfettered access to domestic capital markets and private capital, a situation that would undermine Beijing’s control of China’s business elites. Without the possibility of market disruption, these enormous investments merely exacerbate China’s overcapacity problem. Money is funneled into those products that can be scaled most rapidly, forcing manufacturers to overproduce and then survive on the slim margins that can be reaped from dumping onto the international market.

THE AGONY OF EXCESS

In industry after industry, China’s chronic overcapacity is creating a complicated dilemma for the United States and the West. In recent months, Western officials have stepped up their criticisms of Beijing’s economic policies. In a speech in May, Lael Brainard, the director of the Biden administration’s Council of Economic Advisers, warned that China’s “policy-driven industrial overcapacity”—a euphemism for antimarket practices—was hurting the global economy. By enforcing policies that “unfairly depress capital, labor, and energy costs” and allow Chinese firms to sell “at or below cost,” she said, China now accounts for a huge percentage of global capacity in electric vehicles, batteries, semiconductors, and other sectors. As a consequence, Beijing is hampering innovation and competition in the global marketplace, threatening jobs in the United States and elsewhere, and limiting the ability of the United States and other Western countries to build supply chain resilience.

At their meeting in Capri, Italy, in April, members of the G-7 warned, in a joint statement, that “China’s non-market policies and practices” have led to “harmful overcapacity. ” The massive inflow of cheap Chinese-manufactured products has already raised trade tensions. Since 2023, several governments, including those of Vietnam and Brazil, have launched antidumping or antisubsidy investigations against China, and Brazil, Mexico, Turkey, the United States, and the European Union have imposed tariffs on various imports from China, including but not limited to electric vehicles.

“Beijing’s industrial policies have driven cities and regions across China into debt”

Faced with mounting international pressure, Xi, leading party journals, and Chinese state media have consistently denied that China has an overcapacity problem. They maintain that the criticisms are driven by an unfounded U.S. “anxiety” and that China’s cost advantage is not the product of subsidies but of the “efforts of enterprises” that “are shaped by full market competition.” Indeed, Chinese diplomats have maintained that in many emerging technology industries, the global economy suffers from significant capacity shortages rather than excess supply. In May, the People’s Daily, the official party newspaper, accused the United States of using exaggerated claims about overcapacity as a pretext for introducing harmful trade barriers meant to contain China and suppress the development of China’s strategic industries.

Nonetheless, Chinese policymakers and economic analysts have long acknowledged the problem. As early as December 2005, Ma Kai, then the director of China’s National Development and Reform Commission, warned that seven industrial sectors, including steel and automobiles, faced severe overcapacity. He attributed the problem to “blind investment and low-level expansion.” Over the nearly two decades since, Beijing has issued more than a dozen administrative guidelines to tackle the problem in various sectors, but with limited success. In March 2024, an analysis by Lu Feng, of Peking University, identified overcapacity problems in new-energy vehicles, electric-vehicle batteries, and legacy microchips. BloombergNEF has estimated that China’s battery production in 2023 alone was equal to total global demand. With the West adding production capacity and Chinese battery makers continuing to expand investment and production, the global problem of excess supply will likely worsen in the years to come.

Lu warned that China’s overdevelopment of these industries will pressure Chinese firms to dump products on international markets and exacerbate China’s already fraught trade relations with the West. To address the problem, he proposed a combination of measures that the Chinese government has already attempted—such as stimulating domestic spending (investment and household consumption)—and those that many economists have long argued for but which Beijing has not done, including separating government from business and reforming redistribution mechanisms to benefit households. Yet these proposed solutions fall short of addressing the fundamental coordination problem plaguing the Chinese economy: the duplication of local government investments in state-designated priority sectors.

LOWER FENCE, TIGHTER LEASH

Thus far, the United States has responded to China’s overcapacity challenge by imposing steep tariffs on Chinese clean energy products, such as solar panels, electric vehicles, and batteries. At the same time, with the 2022 Inflation Reduction Act, the Biden administration has poured billions of dollars into building U.S. domestic capacity for many of the same sectors. But the United States should be wary of trying to isolate China simply by building trade barriers and beefing up its own industrial base.

By offering large incentives to companies that invest in critical sectors in the United States, Washington could replicate some of the same problems that are plaguing China’s economy: a reliance on debt-fueled investment, unproductive resource allocation, and, potentially, a speculative bubble in tech-company stocks that could destabilize the market if it suddenly burst. If the goal is to outcompete Beijing, Washington should concentrate on what the American system is already better at: innovation, market disruption, and the intensive use of private capital, with investors choosing the most promising areas to support and taking the risks along with the rewards. By fixating on strategies to limit China’s economic advantages, the United States risks neglecting its own strengths.

U.S. policymakers also need to recognize that China’s overcapacity problem is exacerbated by Beijing’s pursuit of self-sufficiency. This effort, which has been given major emphasis in recent years, reflects Xi’s insecurity and his desire to reduce China’s strategic vulnerabilities amid growing economic and geopolitical tensions with the United States and the West. In fact, Xi’s attempts to mobilize his country’s people and resources to build a technological and financial wall around China carry significant consequences of their own. A China that is increasingly cut off from Western markets will have less to lose in a potential confrontation with the West—and, therefore, less motivation to de-escalate. As long as China is tightly bound to the United States and Europe through the trade of high-value goods that are not easily substitutable, the West will be far more effective in deterring the country from taking destabilizing actions. China and the United States are strategic competitors, not enemies; nonetheless, when it comes to U.S.-Chinese trade relations, there is wisdom in the old saying “Keep your friends close and your enemies closer.”

The U.S. government should discourage Beijing from building a wall that can sanction-proof the Chinese economy. To this end, the next administration should foster alliances, restore damaged multilateral institutions, and create new structures of interdependence that make isolation and self-sufficiency not only unattractive to China but also unattainable. A good place to start is by crafting more policies at the negotiation table, rather than merely imposing tariffs. Waging trade wars amid geopolitical tensions will heighten the confidence deficit in the Chinese economy and lead to the depreciation of the renminbi, which will partly offset the impact of tariffs.

China may also be more flexible in its trade policies than it appears. Since the escalation of the U.S.-Chinese trade war, in 2018, Chinese scholars and officials have explored several policy options, including imposing voluntary export restrictions, revaluing the renminbi, promoting domestic consumption, expanding foreign direct investment, and investing in R & D. Chinese scholars have also examined Japan’s trade relations with the United States in the 1980s, noting how trade tensions forced mature Japanese industries, such as automobile manufacturing, to upgrade and become more competitive with their Western rivals, an approach that could offer lessons for China’s electric-vehicle industry.

Apart from voluntary export restrictions, Beijing has already tried several of these options to some extent. If the government also implemented voluntary export controls, it could kill several birds with one stone: such a move would reduce trade and potentially even political tensions with the United States; it would force mature sectors to consolidate and become more sustainable; and it would help shift manufacturing capacity overseas, to serve target markets directly.

“Xi is attempting to build a technological and financial wall around China”

So far, the Biden administration has taken a compartmentalized approach to China, addressing issues one at a time and focusing negotiations on single topics. In contrast, the Chinese government prefers a different approach in which no issues are off the table and concessions in one area might be traded for gains in another, even if the issues are unrelated. Consequently, although Beijing may seem recalcitrant in isolated talks, it might be receptive to a more comprehensive deal that addresses multiple aspects of U.S.-Chinese relations simultaneously. Washington should remain open to the possibility of such a grand bargain and recognize that if incentives change, China’s leadership might shift tactics abruptly, just as it did when it suddenly ended the zero-COVID policy.

Washington should also consider leveraging multilateral institutions such as the World Trade Organization to facilitate negotiations with Beijing. For example, China might agree to voluntarily drop its developing country status at the WTO, which gives designated countries preferential treatment in some trade disputes. It may also be persuaded to support a revised WTO framework to determine a country’s nonmarket economy status—a designation used by the United States and the EU to impose higher antidumping tariffs on China—on an industry-by-industry basis rather than for an entire economy. Such steps would acknowledge China’s economic success, even as it held it to the higher trade standards of advanced industrialized countries.

Xi views himself as a transformational leader, inviting comparisons to Chairman Mao. This was evident when he formally hosted former U.S. Secretary of State Henry Kissinger—among the few widely respected American figures in Xi’s China—in July 2023, just four months before Kissinger’s death. Xi believes that as a great power, his country should not be constrained by negotiations or external pressures, but he might be open to voluntary adjustments on trade issues as part of a broader agreement. Many members of China’s professional and business elite feel despair about the state of relations with the United States. They know that China benefits more by being integrated into the Western-led global system than by being excluded from it. But if Washington sticks to its current path and continues to head toward a trade war, it may inadvertently cause Beijing to double down on the industrial policies that are causing overcapacity in the first place. In the long run, this would be as bad for the West as it would be for China.

ZONGYUAN ZOE LIU is Maurice R. Greenberg Fellow for China Studies at the Council on Foreign Relations and the author of Sovereign Funds: How the Communist Party of China Finances Its Global Ambitions.

Original article: Foreign Affairs